Cryptocurrency Ifrs 9

Cryptocurrency is an asset for sure because asset is a resource controlled by an entity as a result of past event from which future economic benefits are expected to flow to the entity that is fully met. Why the new standard.

Analytics Ifrs 9 2 Infogram Charts Infographics Management Infographic Analytics Infographic

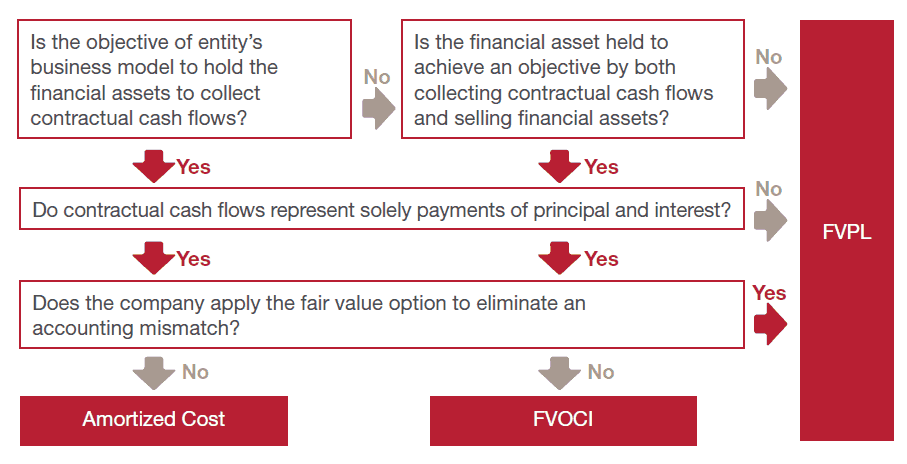

We believe that this would produce our preferred accounting of fair value through profit and loss due to the asset failing the solely payment of principal and interest test needed to apply amortised cost measurement.

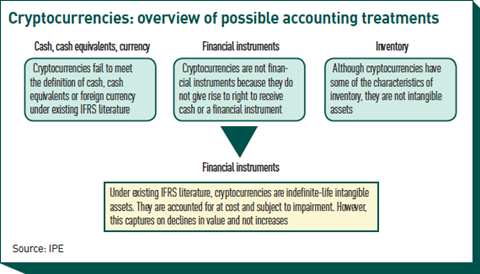

Cryptocurrency ifrs 9. Many cryptocurrencies have grown to be digital alternatives to fiat currency and investments and are closer in nature to financial instruments than intangible assets such as patents or research and development. Are cryptocurrencies inventory Quick read cryptocurrency IFRS reporting Entities holding cryptocurrency Best intro to accounting for. As a result of the foregoing the IFRS Interpretations Committee in its Agenda paper 12 of its June 2019 update observed that a holding of cryptocurrency meets the definition of an intangible asset in IAS 38 on the premises that cryptocurrencies are capable of being separated from the holder and sold or transferred individually.

Executive summary 2 IFRS Viewpoint 9. IFRS 13 defines an active market and judgement should be applied to determine whether an active market exists for particular cryptocurrencies. Such a crypto-asset will be subject to the IFRS 9 classification and measurement requirements.

Therefore it does not appear that digital currencies represent cash or cash equivalents that can be accounted for in accordance with IAS 7. Cryptocurrency assets are acquired by the reporting entity with the purpose of selling them in the near future and generating a profit from fluctuations in price or broker-traders margin. Measurement models de fined by IFRS 9 a finan cial asset at fair value t hrough.

IFRS IC to consider guidance for the accounting of transactions involving cryptocurrencies possibly in the form of an agenda decision on how an entity might walk through the existing IFRS requirements. And cryptocurrencies do not give the holder a right to receive a fixed. Those crypto-assets that are meant to constitute a peer-to-peer alternative to government-issued fiat currency.

IFRS 9 notes that although gold bullion is highly liquid there is no contractual right to receive cash or another financial asset inherent in bullion and is therefore not a financial instrument. A general-purpose medium of exchange independent of any central bank. However in late 2016 the IASB agreed to provide entities whose predominate activities are insurance related the option of delaying implementation until 2021.

Being a store of value a unit of account and a medium of exchange 10. However there may be limited circumstances in which cryptocurrencies are 1 held for sale in the ordinary course of business and thus considered inventory as in the case of a broker or 2 accounted for as an investment by an. IFRS 9 replaces IAS 39.

For the reasons explained below we believe that cryptocurrencies should generally be accounted for as indefinite-lived intangible assets under ASC 350. Cryptocurrencies are not equivalent to fiat currencies because they do not meet the three defining criteria of money ie. Cryptocurrencies can no longer apply IFRS 9 Financial Instruments or IAS 8 Accounting Policies Changes in Accounting Estimates and Errors when accounting for cryptocurrencies.

IFRS 9 generally is effective for years beginning on or after January 1 2018 with earlier adoption permitted. Oct 16 2018 At its meeting on October 16 2018 the IFRS Discussion Group IDG discussed the accounting for transactions whereby an entity receives services from both non-employees and employees in exchange for a type of cryptocurrency that carries the right to transfer to another party eg Bitcoin Ethereum and Litecoin. Nov 14 2018 At its meeting on November 14 2018 the IASB met to consider information provided by the IFRS Interpretations Committee Committee about how an entity might apply existing IFRS Standards to account for holdings of cryptocurrencies and initial coin offerings.

Cryptocurrencies International Accounting Standards Board Date recorded. These were the first types of crypto-assets to emerge rising to. Where the revaluation model can be applied IFRS 13 Fair Value Measurement should be used to determine the fair value of the cryptocurrency.

July 2018 1 Refers to a programming style that does not include any shortcuts to improve performance but instead relies on sheer computing power to try all possibilities until the solution to a problem is found. All financial assets are initially recorded at fair value plus attributable transaction costs apart from those subsequently measured at fair value through profit or loss in which case the transaction costs should be expensed as incurred. Intuitively it might appear that cryptocurrency should be accounted for as a financial asset at fair value through profit or loss FVTPL in accordance with IFRS 9.

In June 2019 the IFRS IC published its agenda decision on Holdings of Cryptocurrencies. Regulators prefer the term crypto-assets to describe cryptocurrencies used for investment purposes and. In IFRS Viewpoint No9 Accounting for cryptocurrencies the basics.

Presently IFRS 9 defines financial instruments categorically rather than conceptually. In accordance with IFRIC decision cryptocurrency meets the definition of intangible asset in line with the standard IAS 38 Intangible Assets. Crypto-assets experienced a breakout year in 2017.

Bitcoin ifrs 9. Highlights In June 2019 in response to a request from the International Accounting Standards Board IASB or the Board the IFRS Interpretations Committee IFRS IC. In our view a simple change to IFRS that would greatly enhance the relevance of financial statements would be to scope cryptocurrencies into IFRS 9.

Cryptocurrencies such as bitcoin and ether have seen their prices surge as the publics awareness has increased and financial market participants have thus increasingly turned their attention to the phenomenon. What differentiates them from traditional investments and why it matters. 2 IFRS Viewpoint 10.

Cryptocurrencies IDG Date recorded.

Getting Ready For Ifrs 9 Accounting Standards Bloomberg Professional Services Risk Management Accounting Accounting Career

Ifrs 9 Stage 1 Ecl Estimation Eloquens

How To Account For Own Use Commodity Contracts Under Ifrs Cpdbox Answers Youtube

Contemporary International Business In The Asia Pacific Region Other Walmart Com In 2021 Economics Books Employee Development International Students

Pdf Accounting For Bitcoin And Other Cryptocurrencies Under Ifrs A Comparison And Assessment Of Competing Models

Let S Learn About Ifrs With Ilearn For Free Ifrs Is The International Accounting Framework Wit Financial International Accounting Professional Accounting

6 Forces Shaping The Future Of The Finance Function Pwc Via Mikequindazzi Rpa Bigdata Dataanalytics Automati Finance Function News Finance Finance

How Well Is Your Board Managing Risk Discussion Strategies Cryptocurrency News Bitcoin

Impairment Profile For Financial Assets Under Ifrs 9

Accounting Matters To Virtually Toss A Coin Or Not Features Ipe

6 Forces Shaping The Future Of The Finance Function Pwc Via Mikequindazzi Rpa Bigdata Dataanalytics Automati Finance Function News Finance Finance

Pdf Free Accounting Principles Ifrs Version Global Edition Buku

Accounting For Cryptocurrencies Under Ifrs Youtube

Ifrs 9 Classification And Measurement Of Financial Instruments Annualreporting

Overcoming Ifrs Adoption Challenges With Smart Contract Development Development Overcoming Financial Information

Pin On Trading Ideas And News

Pdf Accounting For Bitcoin And Other Cryptocurrencies Under Ifrs A Comparison And Assessment Of Competing Models

Fix Missing Figures In Cash Flow Statement Cash Flow Statement Fundamental Analysis Cash Flow

Download Ifrs 9 And Cecl Credit Risk Modelling And Validation A Practical Guide With Examples Worked In R And Sas Kindle Sas Accounting Principles Practice

Comments

Post a Comment